Contents

Cost Inflation Index (CII) – What is CII & Who notifies CII

‘Cost Inflation Index’ (CII) for any year means such index as the Central Government may, having regard to seventy-five percent of the average rise in the consumer price index for the urban non-manual employees for the immediately previous year to such previous year.

Central Government publishes CII by notification in Official Gazette.

CII = 75% x Average rise in Consumer Price Index (CPI) for Urban non-manual employees.

Why Cost Inflation Index (CII) is calculated

CII is calculated to factor in the inflation in purchase prices.

The use of the Cost Inflation Index (CII) is calculated.

CII is used to increase the original purchase price after factoring in inflation as notified by Government in this regard. To benefit the taxpayers, CII benefits are applied to long-term capital assets to cost the price of an asset by factoring inflations; thereby, the capital gain value is rationalized; otherwise, the taxpayer would have to pay higher capital gain tax.

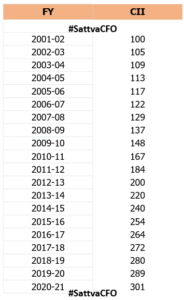

Year-wise Cost Inflation Index – CII

The year-wise Cost Inflation Index is as follows:

The base year is the Cost Inflation Index – CII.

Base Year is the first year of the Cost Inflation Index, i.e. FY 2001-02 is 100. Index of all year is compared to a base year to find the increase in inflation.

Latest Cost Inflation Index (CII) for FY 2021-22 / AY 2022-23

The Cost Inflation Index (CII) for AY 2022-23 / FY 2021-22 is 317.

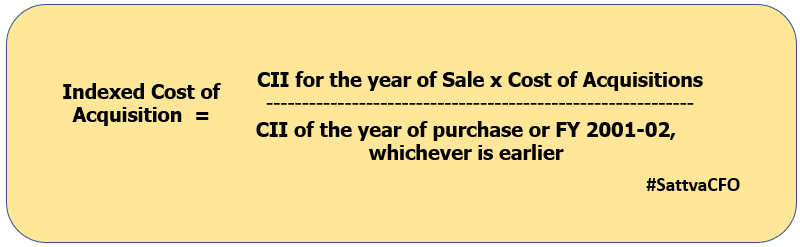

How is the indexed cost of acquisition calculated?

Indexed cost of acquisition is calculated by the following formulae:

Leave a Reply